Unit-linked versus euro funds

Reading time: 3 min

| Euro Fund | Units of account | |

|---|---|---|

| Cover | Total premiums paid (denominated in foreign currency) minus the costs of the policy | Number of units of account |

| Financial risk | Supported by the insurance company | Supported by the subscriber |

| Underlying | Mostly government and corporate bonds | All types of financial assets authorised by the insurance company |

| Return/performance | Extremely limited, linked to the composition of the euro fund, the fall in government bond yields and the insurance company's policy on profit distribution | Potentially unlimited, depending on the performance of the policy’s underlying assets |

| Investment strategy | Limited to the insurance company's strategy for the management of the euro fund | Customisation of the strategy depending on the client's investment objectives |

| Investment limits | Limited to the part of the premium invested in euro funds by the insurance company | No investment limits (except for the choice of specific assets) |

| Exit penalties |

Potential exit penalties in the event of early surrender (according to the company's euro fund) |

In practice, there is no exit penalty for the policy’s underlying investments |

Do you wish to have more information?

Contact us

The contents of this theme

Reading time: 3 min

Unit-linked versus euro funds

7 points of comparison between euro funds and units of account.

Reading time: 3 min

The advantages of unit-linked policies

The advantages of the life insurance contract include a high degree of flexibility and security.

Reading time: 3 min

Statistics on Unit-Linked Policies

Luxembourg, leader in the management of unit-linked life insurance contracts.

Reading time: 3 min

The various available investment vehicles

The diversity of the investment vehicles of the Luxembourg life insurance contract explained in video infographics.

Reading time: 2 min

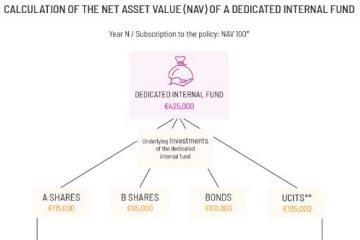

Calculation of the NAV of an internal dedicated fund

How is the net asset value of a dedicated fund calculated?

Euro funds or units of account? Which solution for your life insurance contract?

The euro fund and units of account are both eligible investments within a Luxembourg life insurance policy. The euro fund offers a guarantee of the premiums paid (less the contract fees), unlike units of account whose performance is linked to the underlying assets of the contract. The unit-linked life insurance contract offers greater flexibility in terms of the type of eligible financial assets and customisation of the strategy according to the risk profile of the policyholder.